REFERRAL PERKS®

Earn $100* for you and your friend for every successful referral.

Debt. For most people, the four-letter word can cause hearts to pound and minds to race. But the truth is that not all debt has to be intimidating. While it may sound counterintuitive, borrowing money can help you achieve your financial goals. The key lies in distinguishing between good debt and bad debt.

What is debt? Put simply, debt is money that’s borrowed for a financial need in exchange for interest.

First, let’s start with the positive. Generally speaking, if debt increases your net worth or helps create future value in your life, it’s considered to be good debt.

Some examples include student loans, mortgages or business loans. That’s because student loans have the power to increase your earning potential over the long term. A house not only puts a roof over your family’s head, but it typically appreciates in value with time. And a business loan can pay off in spades by allowing you to increase your cash flow dramatically.

![]()

One of the things we all need to do is decide how much we're comfortable having in a monthly payment outflowing from our paychecks, which could be different from what you can afford on paper.

- Alex Brocklebank , Branch Manager

Bad debt, on the other hand, refers to credit cards, payday loans or other consumer debt that does little to improve your financial outcome. These are often used for unnecessary purchases beyond one’s means, such as expensive clothing or extravagant meals. You'll be saddled with high-interest fees if these aren’t paid off each month. And that can impact your credit score and financial health.

Cars and boats are purchases that often spark confusion. These are depreciating assets — meaning that they typically fall into the bad debt camp. However, if you use a vehicle to get to work each day to earn an income, it can be considered good debt.

A helpful way to separate good from bad debt is to ask yourself: Will the debt give you more back than you initially put in?

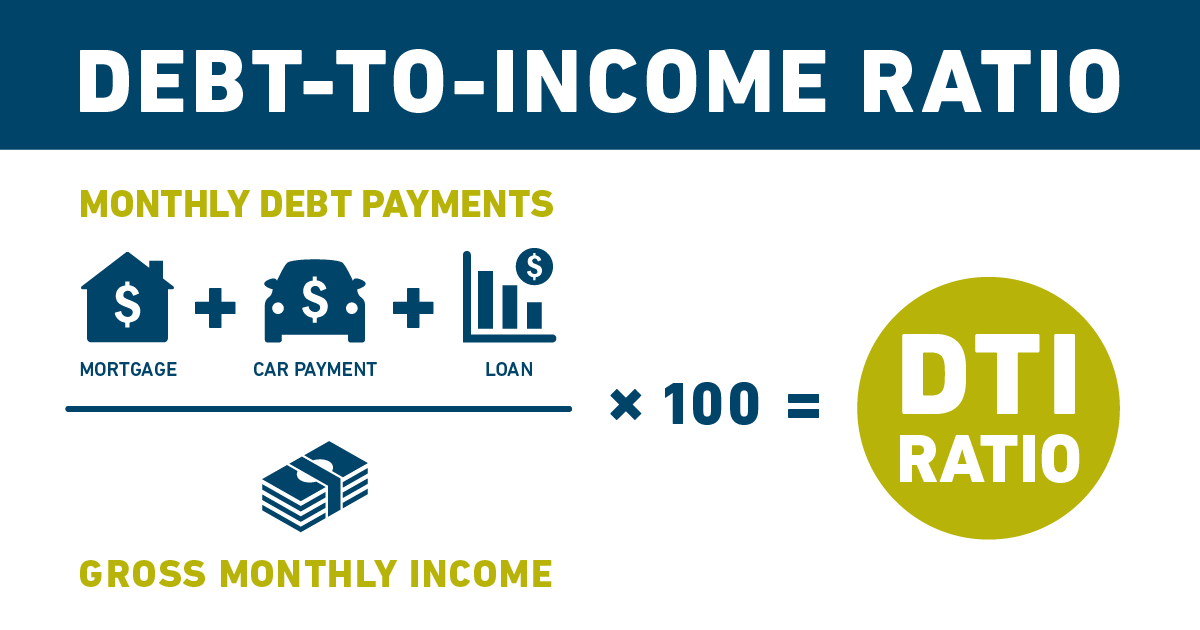

Now that we’ve distinguished good debt from bad debt, how do you know how much you can carry to get ahead financially? A handy tool to determine this is the debt-to-income ratio, which is essentially your earnings compared to the debt you owe each month. A good rule of thumb is to ensure that your debt is no more than 44% of your gross monthly income.

So, say you have a $1,400 mortgage, a $400 car payment and $200 in student loans, for a total monthly debt of $2,000 — along with a gross monthly income of $4,000. Then your debt-to-income ratio is 50%. This means half of your income is going toward your debt, which is considered a red flag for lenders and a sign that you’re borrowing more than you can afford.

It’s recommended to have a debt-to-income ratio that’s below 44%.

Not all debt is bad. Borrowing money can help you get ahead if it’s used to purchase assets that increase in value over time — like paying for an education or funding a new business venture. Most importantly: use the debt-to-income ratio to evaluate how much debt you can safely borrow.

Speak to an advisor on the phone or at a branch.

We acknowledge that we have the privilege of doing business on the traditional territory of First Nations communities.